Precious metals are apparently waking up. And here is where you can find the best deals.

Site:

Precious metals news

Donald Trump and Chinese Vice Premier Liu inked their signatures on the Phase 1 trade deal this week. But was it really a big deal? Or was it no deal? Mike Maharrey talks about it on this week's Friday Gold Wrap podcast. He also talks about why the gold market seems to be holding steady despite some strong headwinds and the outlook for the yellow metal in 2020.

Mnuchin is again talking about how it might be a good time for the government to issue ultra-long bonds, or those with 50- and 100-year maturities, given that yields are at or near record lows.

China's economic growth cooled to its weakest in nearly 30 years in 2019 amid a bruising trade war with the U.S., & more stimulus is expected this year as Beijing tries to boost sluggish investment and demand.

And things could get really scary. Lenders, mortgage services, investors & homeowners should prepare for trouble in the mortgage market.

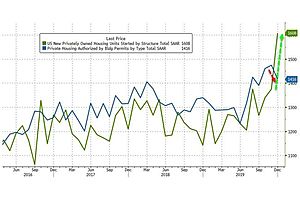

Multi-family starts soared 75% YoY... welcome to renter nation!

The central bank’s short-term buying of securities could morph into long-term easing.

In the court of investor opinion, the verdict is in. The Fed is guilty of quantitative easing. Never mind that Chairman Jerome Powell tells everyone his efforts to shore up funding markets are “in no sense” QE. Try as policy makers may, they’ve lost the ability to convince people...

"These risks could inflict severe and long-lasting damage on development prospects."

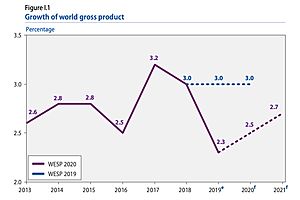

IMF: The U.S.’s momentum will fall behind that of the rest of the world as global growth bottoms out and looks set to slowly pick up in 2020.

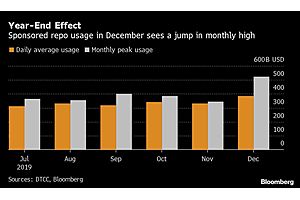

The Fed was victorious in preventing a year-end squeeze in funding markets. But it had a little help from its friends.A $276 billion surge in the use of so-called sponsored repo from money market funds in December helped banks open their lending taps and add to the $256 billion...

Liquidity driven momentum rallies can keep going beyond all reason or fundamental basis, that’s what bubbles are all about. The Fed knows what it’s doing and keeps insisting on doing it:

The most probable scenario for the global economy and financial markets this year is fairly obvious: continued GDP growth, rock-bottom interest rates, and rising equity prices. It's more useful to identify which unlikely events would alter this likely benign scenario – and consider how unlikely they really are.

The Credit Suisse global strategy team’s annual surprise predictions include a surge in U.S. stocks and a bursting of the Chinese bubble.

Central banks will try and resolve the debt burden through currency depreciation (inflation), and China has been preparing for this...

January 16, 2020

This chart likely proves 100% what's going on...

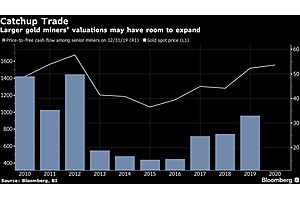

Gold’s blistering rally isn’t over, according to fund managers who see another leg up for the precious metal.Lower-for-longer interest rates, a weaker dollar and the U.S. presidential election will provide multiple catalysts for gains, even as tentative trade peace breaks out...

America is weaponizing its currency and financial system.

Lance Roberts: The problem with low interest rates for so long is they have encouraged the misallocation of capital.

Now that we are no longer pretending that the Fed's "NOT QE" is not in fact "QE 4", investors and strategists are starting to look more carefully at how the Fed is monetizing the T-Bills as part of its market boosting reserve management Permanent Open Market Operation remit.

Some European Central Bank officials warned at their latest policy meeting about the possible adverse side effects of negative interest rates, according to minutes of the meeting, raising questions about the future of a key policy tool.