Gold has all the potential to go unprecedentedly high. But silver will be gold on

Site:

Precious metals news

**Ancient Rome and Today's Currency Challenges:**

Central Italy's bronze was to early Rome what traditional currencies are to us now. As Rome expanded, it integrated precious metals, much like today's interest in gold reserves. The denarius, introduced in 211BC, can be likened to a dominant global currency today. As Rome transitioned to Empire, they debased the denarius to finance their expenses, reminiscent of some modern nations printing money, leading to inflation. Despite this, Rome insisted on taxes in pure metals, echoing how some countries still demand debt payments in strong currencies. This unsustainable strategy, paired with overextension like some economies today, signaled Rome's financial downfall.

Reliance on constant borrowing and fiscal stimulus is masking the real issues within the economy. While we're flooded with narratives of economic growth, low unemployment, and rising wages, the underlying foundation is shaky. The belief that central banks and governments can endlessly borrow and spend to fix any problem is misguided. This overconfidence in financial solutions overlooks the real-world consequences, such as debt-induced inflation, increasing wealth inequality, and stagnating economic growth. As more money is thrown at these issues, diminishing returns are evident, and problems are exacerbated instead of resolved. The ever-growing mountain of debt and its consequent interest payments eventually suffocate genuine investment and consumption. Relying solely on financial "tricks" distorts the economy's capacity to address genuine challenges. Eventually, reality will catch up, potentially leading to a market crash and systemic collapse. Blind faith in perpetual borrowing and spending is a dangero...

China's economy teeters on the brink of disaster, and its impending collapse could blow up the global economy. The once-mighty real estate sector is in ruins, with titans like Evergrande and Country Garden sinking under insurmountable debts. Liquidity crises are widespread, with firms like Zhongzhi on life support. The Chinese government's move to obscure crucial data adds to the growing mistrust and suspicion about the true extent of the debacle. The frantic rate cuts by the People's Bank of China scream panic, yet there's a conspicuous absence of a strong stimulus to stabilize the situation. With the warning bells for China's economic implosion ringing loud, diving into its equities is akin to playing with fire.

Aug 18, 2023 - 11:57:18 PDT

Wall Street expert Jeremy Grantham predicts that rising interest rates will lead to a recession, contradicting the Federal Reserve's optimistic outlook. He remarked that the Fed has a history of missing recession signals, especially after major market bubbles. Grantham believes the tech stock decline's deflationary effects will combine with the impact of higher rates on sectors like real estate, causing a prolonged economic downturn and stock price drop. He anticipates the S&P 500 to drop significantly by year-end and sees a future of consistently higher inflation and interest rates. In essence, low rates boost asset prices, while high rates depress them.

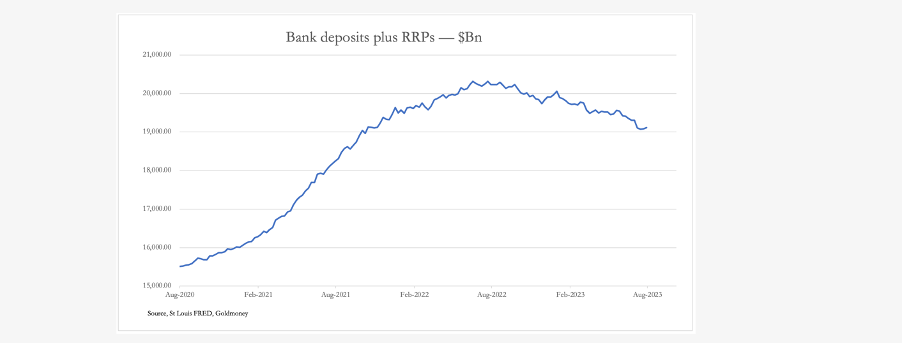

The sell-off in precious metals which started in late July continued this week, but its momentum slowed with silver even showing a modest gain on the week so far. In early European trading, gold was $1892, having traded down to $1885 yesterday, for a net fall of $19 on the week. Silver was $22.78 having traded down to $22.30 on Tuesday but is up just 10 cents from last Friday’s close. On Comex, turnover in the gold contract was subdued, but in silver it was moderate to healthy.In silver, the Commitment of Traders report for 8 August showed the Managed Money category was net short 3,781 contracts, with very low levels of longs and shorts making the balance. It seems that the trading community has withdrawn from this contract. And the Swaps unusually are sitting on net longs of 499 contracts. It is the Non-Reported category which has sold down its net long position. This is up next.With Open Interest on Comex being low (it has been lower recently, down to 114,421 on 3 J...

A staggering 61% of Americans are living paycheck to paycheck, struggling to cover essential living expenses, as per a LendingClub report. Moreover, 72% feel financially insecure, and over a quarter believe they'll never achieve financial stability, according to Bankrate. This financial strain isn't new; since 1979, wage growth for the bottom 90% has been a mere 15% compared to the top 1%'s 138% surge. With the recent concerns about inflation and rising interest rates, this issue is magnified. The average worker's take-home pay is approximately $3,308 monthly. Yet, the median rent takes up about 61% of this, and essential expenses like food and health further strain budgets.

Aug 18, 2023 - 08:45:21 PDT

The Biden administration's revision of the Davis–Bacon Act of 1931 may have detrimental effects on the economy, inflating the costs of federal projects. This act, which determines prevailing wages on public works projects, now allows state and local governments to set these wages. Such a shift seems poised to benefit states with union-heavy influences, potentially skyrocketing costs. This extended mandate will impact projects like broadband and solar panels that are partly federally funded. This inflationary move, combined with other financial policies under this administration, could push the country into an economic pitfall. The continued trajectory of such policies may set the stage for a prolonged inflation nightmare.

Aug 18, 2023 - 07:20:36 PDT

Global stock markets faced severe declines this week due to concerns over China's economic slowdown and high U.S. interest rates. Hong Kong's Hang Seng index plunged into bear market territory after Chinese property giant Evergrande declared bankruptcy protection in the U.S., triggering broad losses in Asia-Pacific stocks. The Stoxx 600 and U.S. stock futures also fell, with the Dow Jones marking its worst week since March. Emmanuel Cau of Barclays described the situation as a "perfect storm" for markets.

Aug 18, 2023 - 06:27:44 PDT

Wermuth Asset Management warns of an impending risk of deflation in the US due to declining stock and real estate values. Despite recent inflation figures, the firm cites the vulnerability of the overpriced stock market and commercial real estate debt nearing $1.5 trillion in maturity. Economist Dieter Wermuth believes the focus should shift from inflation to deflation risks, especially with the S&P 500 being "dangerously overpriced" and potential troubles in the commercial real estate market. The firm anticipates central banks will recognize deflation as the primary concern by September.

Aug 18, 2023 - 06:20:20 PDT

Scott Rechler, CEO of RXR Realty, warned of significant losses for banks and investors as many office buildings become obsolete. While top-tier Class A buildings will prosper, lower-tier buildings face potential obsolescence. The US office vacancy rate recently hit an all-time high of 13.1%. Goldman Sachs and other banks are buying distressed properties, anticipating a drop in prices. With $1.5 trillion of debt in the commercial real estate sector nearing maturity and banks reducing lending, experts predict a possible commercial real estate crash, with office prices potentially dropping by 35% in the coming decades.

Economic experts weigh in on looming economic risks:

- **Chetan Ahya, Morgan Stanley**: Fears a US recession and a substantial deceleration in China's growth rate, especially if both occur simultaneously.

- **Mohammed Al-Jadaan, Saudi Arabia’s finance minister**: Sees fragmentation and increasing trade restrictions as the top threats, disrupting supply chains and spiking costs.

- **Olivier Blanchard, Former IMF chief economist**: Believes that although the battle against inflation might cause temporary recessions, geopolitical tensions, like subsidy and tariff wars, pose a more lingering concern.

- **Ethan Harris, Former Bank of America Corp. economist**: Highlights the risk of major geopolitical shocks, including potential US-China economic decoupling and persistent high inflation.

- **Alicia Garcia Herrero, Natixis SA**: Pinpoints the uncoordinated industrial policies between major nations that jeopardize emerging and developing countries' growth aspirations.

- **Zhang Jun, Fudan University**: Warns aga...

San Francisco's housing market is showing alarming signs of decline, with the median price of single-family homes plummeting by 8.5% in July compared to June, marking a 14.1% drop from last year. Since its peak in March 2022, prices have collapsed by a staggering 29%. This trend parallels the 2007 housing bust, though current indicators suggest an even sharper descent this time. The broader Bay Area also isn't immune, experiencing a 5.2% drop in July, with a 16.3% plunge since April 2022.

There is a growing consensus that the Federal Reserve can successfully slay price inflation and bring the economy to a soft landing. After all, the economy appears to be chugging along. But as Friday Gold Wrap host Mike Maharrey explains, there are a lot of things bubbling under the surface that should temper that optimism. In fact, what we're seeing today looks a lot like 2007.

Aug 17, 2023 - 12:50:20 PDT

The US LEI has seen its 16th consecutive decline, echoing the dire trends of the 2007-2008 Lehman crisis. Despite the CEI's subtle stability, July's significant LEI drop, spurred by weak orders and rising interest rates, portends a bleak economic horizon. The 7.5% year-on-year LEI descent is nearing its worst since 2008, excluding COVID anomalies. The Conference Board anticipates a recession between Q4 2023 and Q1 2024, dispelling hopes of a 'soft landing' for the US economy.

Iran and Russia's Central Banks are exploring a gold-backed "stable coin" to supplant the US dollar in trade, especially beneficial in Astrakhan's Special Economic Zone. Sergey Glazyev suggests a new pricing strategy: "Fixing the price of oil in gold at the level of 2 barrels per 1g will give a second increase in the price of gold in dollars," according to Credit Suisse's Zoltan Pozsar. This acts as a solid counter to Western 'price ceilings'. Glazyev's approach is gaining attention, potentially laying the groundwork for a "G7 of the East" with the current BRICS nations at its core. As global trade dynamics evolve, such a gold-backed currency could drastically alter the world's financial status quo.

The Argentina peso, already this year's weakest global currency, is predicted to plummet further, warns Bank of America Corp. strategists. Expectations are that the rate might sink to 545 per dollar by year's end and drastically tumble to 1,193 by 2024. Following electoral losses, the government devalued the peso by 18%, exacerbating Argentina's economic challenges. Key concerns include political instability, impending general elections, inflation, and mounting national debt.

Aug 17, 2023 - 11:56:18 PDT

The IMF lists the US dollar among its eight primary currencies. Historically backed by gold, today's currencies are now based on devalued paper backed by debt, with the dollar's worth plummeting to 4 cents since 1930. As nations like BRICS hoard gold and seek a return to the gold standard for stability, Western nations deplete their gold reserves. The gold standard would curb excessive government borrowing. With the Federal Reserve's manipulations, the dollar's value has decreased, while gold's value has surged. A push towards digital currency could further erode the traditional financial system, risking the US's economic stability.

BRICS nations are intensifying de-dollarization efforts by settling oil and gas trades in local currencies, threatening the dominance of the U.S. dollar. Ahead of the BRICS summit in Johannesburg, the alliance aims to leverage oil, a global trade linchpin, to promote local currencies. India notably settled crude oil transactions in Rupees with the UAE, while France and Russia have begun transacting in the Chinese Yuan for gas and oil trades respectively. With Saudi Arabia considering the Yuan for oil settlements and eight Arab nations keen to join BRICS, the U.S. dollar's supremacy in global trade could face significant challenges.

Globally, further falls in consumer price inflation are now unlikely and there are yet further interest rate increases to come. Bond yields are already on the rise, and a new phase of a banking crisis will be triggered.This article looks at the factors that have come together to drive interest rates higher, destabilising the entire global banking system. The contraction of bank credit is in its early stages, and that alone will push up interest costs for borrowers. We have an old fashioned credit crunch on our hands.A new bout of price inflation, which more accurately is an acceleration of falling purchasing power for currencies, also leads to higher interest rates. Savage bear markets in financial and property values are bound to ensue, driving foreign investors to repatriate their funds.This will unwind much of the $32 trillion of foreign investment in the fiat dollar which has accumulated in the last fifty-two years. And BRICS’s deliberations for replacing the doll...

Aug 17, 2023 - 09:24:50 PDT

During the 1970s, a period marked by high inflation and economic uncertainty, investors witnessed something extraordinary.